Elliott Sends Letter to Shareholders and Mails Definitive Proxy Materials Outlining Why Board Change is Needed at Phillips 66

Highlights Plan to Improve Performance, Strengthen Accountability and Increase Shareholder Value

Identifies Slate of Four Highly Qualified Independent Director Candidates with Decades of Experience in Refining, Midstream Operations and Corporate Governance

More Information at Streamline66.com

WEST PALM BEACH, FLA. (April 3, 2025) – Elliott Investment Management L.P. (“Elliott”), which manages funds that together have an investment of more than $2.5 billion in Phillips 66 (NYSE: PSX) (the “Company” or “Phillips”), today sent a letter to the Company’s shareholders highlighting why change is urgently needed on the Phillips Board of Directors (the “Board”). In the letter, Elliott made the case that Phillips investors’ patience has been punished, and a new lineup on the Board is necessary to reverse the Company’s long-term underperformance and improve its poor corporate governance practices. Elliott also filed definitive proxy materials in connection with Phillips’ Annual Meeting of Stockholders (the “Annual Meeting”), which is currently scheduled for May 21, 2025.

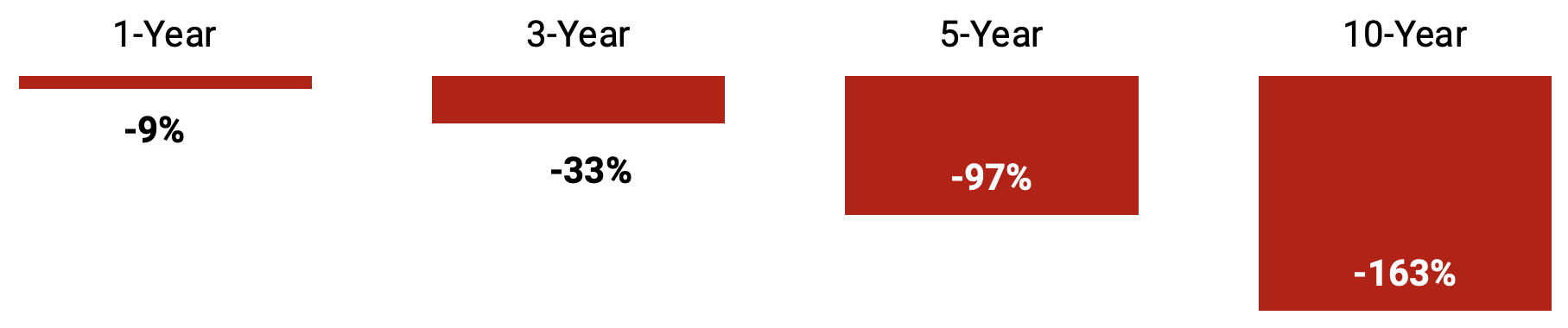

In its materials, Elliott detailed the degree to which Phillips’ operating performance has consistently trailed its industry peers. Notably, over the past decade, Phillips shares have underperformed Valero Energy and Marathon Petroleum, by -138% and -188%, respectively.

In addition, Elliott discussed why its three-part “Streamline 66” plan – which Elliott believes has the potential to increase Phillips’ stock price to more than $200 per share – would be the best path forward. The plan includes a simplification of Phillips’ portfolio, a thorough review of its refinery operations and enhanced oversight of management at the Board level.

Elliott also disclosed its four highly qualified director nominees, who would add urgently needed experience and valuable new perspectives to the Board:

- Sigmund Cornelius served as CFO at the predecessor company of Phillips, ConocoPhillips, where he oversaw a substantial divestiture and simplification program that led to a material increase in shareholder value. He later served as President of Freeport LNG Development, as well as a director at Andeavor and Western Refining.

- Michael Heim has a long record of leadership in the industry as a founder of Targa Resources, one of the most successful Permian-focused midstream operators, and as a member of multiple boards and a respected consultant.

- Brian Coffman is a seasoned operator who spent much of his career running Phillips’ current refining assets while they were part of ConocoPhillips. After three decades at ConocoPhillips, he became the executive in charge of refining for Andeavor, leading the operations of ten refineries throughout the United States, as well as the President and CEO of Motiva, one of North America’s largest refiners.

- Stacy Nieuwoudt would bring an investor’s eye to Phillips’ challenges, having spent her career as a senior energy and industrials analyst at Citadel. She has also served on the boards of multiple publicly traded energy companies.

In addition, Elliott encouraged Phillips’ shareholders to support a proposal calling for all directors to commit to a one-year term and stand for election at each Annual Meeting – a policy that would make all directors accountable to shareholders, every year. Currently, only a portion of Phillips Board seats are up for election each year, and while proposals to address this governance defect have received near-unanimous support at past Phillips Annual Meetings, those proposals have never passed due to the onerous requirement that 80% of all outstanding shares – not just votes cast – be in favor. Phillips has put forward the same proposal for this Annual Meeting.

“The Company is asking shareholders to try the same approach to de-staggering that has repeatedly failed before – fully aware that its supermajority voting requirement makes failing again a near certainty,” Elliott wrote. By contrast, the proposal that Elliott has put forward would require “only that all Phillips 66 directors have the courage to be accountable to shareholders on an annual basis, as is the case at nearly 90% of the companies in the S&P 500.”

“Making this company the best it can be – with a focus on core strengths and operational discipline, overseen by an adept and energetic Board – offers the possibility of a stronger, more valuable Phillips 66 for all of its investors,” the letter concluded.

For more information, including how to vote on Elliott’s GOLD proxy card, please visit Streamline66.com.

The full text of the letter follows:

Dear Fellow Phillips 66 Shareholder:

We are writing to you as fellow investors in Phillips 66 (NYSE: PSX) (the “Company”), an energy conglomerate that is falling well short of its potential and is in urgent need of a new direction.

We believe that with resolute and decisive action, Phillips 66 is primed to deliver far greater returns for its shareholders than it has over the past decade. The purpose of this letter is to seek your support for an upgraded Board of Directors that is committed to achieving the performance that shareholders demand and deserve. Your vote on the enclosed Gold Card will set in motion a clear plan to improve Phillips 66’s operating performance, strengthen Board accountability and increase the value of your investment.

We at Elliott Investment Management L.P. (together with its affiliates, “Elliott”) manage funds that hold a stake of more than $2.5 billion in Phillips 66, making us one of the Company’s largest investors. Founded in 1977, Elliott specializes not just in identifying value, but in helping to create it – by urging companies to shake off corporate complacency, adopt better practices and capitalize on their best opportunities. When the situation demands it, we advocate for new leadership to ensure that the companies in which we invest are serving the best interests of their shareholders.

Unfortunately, Phillips 66’s current leaders have shown a frustrating unwillingness to prioritize shareholder value. They have resisted proposals to improve accountability, and they have declined to fully implement the changes necessary to recover from their long-term underperformance. Instead, Phillips 66 has deployed self-interested and counterproductive defensive maneuvers that serve only to entrench current leadership, while continuing to miss targets and generate disappointing results. A comparison of Phillips 66’s performance to that of its industry peers shows just how far the Company has fallen behind. Consider that over the past decade, Phillips 66 shares have managed to underperform Valero Energy (“Valero”) and Marathon Petroleum (“Marathon”), its closest peers, by -138% and -188%, respectively.1

Phillips 66 Cumulative Total Return vs. Valero and Marathon2

That is no accident: Unlike at Phillips 66, shareholder-focused boards and management teams at those companies have recognized the need for improvement, welcomed investor advice and responded with decisive changes.

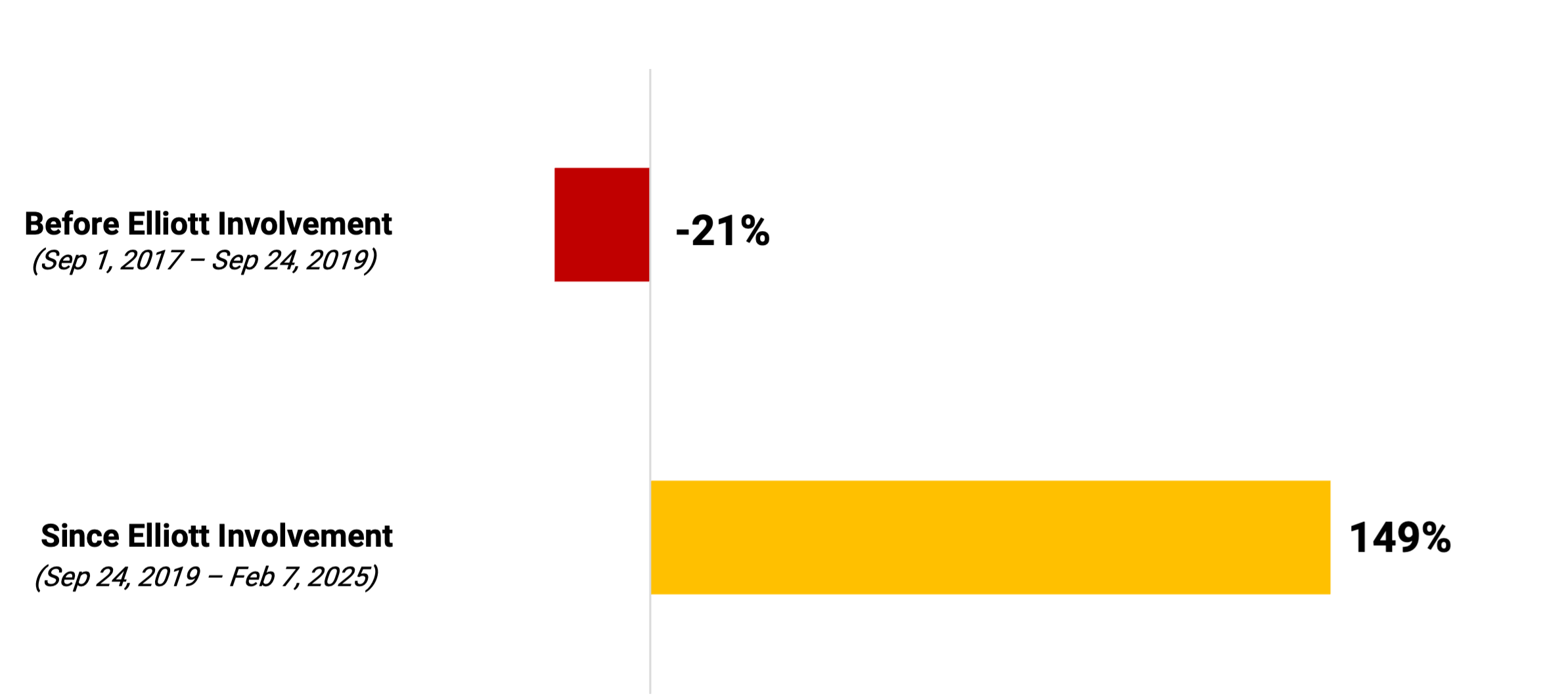

Take Marathon, in which Elliott has been a significant and engaged investor. Marathon has excelled since its board carried out a series of crucial changes that we recommended, resulting in a ~150% relative outperformance by Marathon’s share price.3

Marathon Petroleum Total Shareholder Return vs. Peers4

When we engaged with Marathon in 2019, the company had challenges comparable to those now facing Phillips 66. We helped Marathon address these issues with plans for stronger governance, strategic divestitures and improved operations under new leadership. Marathon soon re-emerged as a standard-setter in the industry – after years of being viewed as a laggard versus best-in-class peer Valero – with results that speak for themselves. Marathon took decisive action and was able to deliver comparable or better profitability per barrel, impressing investors and delivering a stock price that greatly outperformed peers.

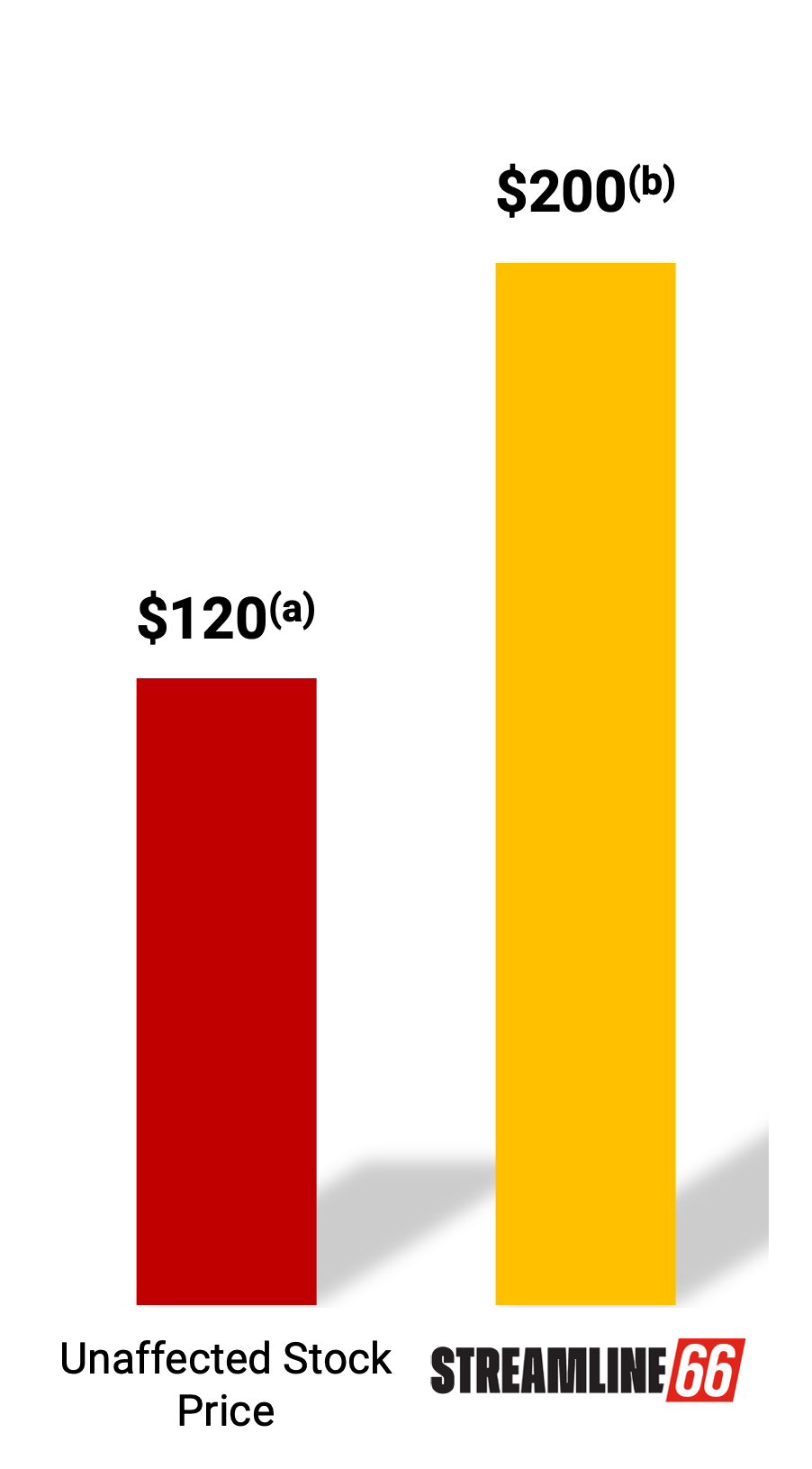

Today, the same kind of turnaround and superlative stock returns are entirely within reach of every Phillips 66 shareholder. In fact, Elliott’s experience with Marathon, and our many other productive engagements with companies in similar situations, make us confident that these steps could lift Phillips 66 shares to $200 or more.5

We view Phillips 66 as positioned to achieve a breakthrough opportunity – but only if it has a leadership team willing and able to turn that potential into the industry’s next big success story.

The “Streamline 66” Plan Could Boost Phillips 66’s Shares to $200+6

Our three-part “Streamline 66” plan starts with simplifying the portfolio to address Phillips 66’s inefficient conglomerate structure and unlock trapped value not reflected in the stock price today.

As currently organized, the Company has refining, midstream, chemicals and other businesses under one roof. These are all high-quality assets, but combining them limits their potential by denying each a focused management team, targeted capital investment and a fully engaged investor base. The aggregation of these disparate businesses into a conglomerate structure has hindered the Company’s performance and weighed down its stock. For Phillips 66 to make the most of its portfolio’s strengths and deliver sustainable returns for its shareholders, it should take the following steps:

- The Company’s midstream business, which we believe could command a valuation of more than $40 billion, should be sold or spun off.7 Its retail operations in Europe, along with its interest in CPChem, a joint venture with Chevron, should also be sold. A divestiture of non-core assets would create a substantial capital return opportunity for Phillips 66 shareholders, while also allowing the management team to concentrate on restoring its lagging refining operations.

- A greater focus on refining is essential at Phillips 66, given recent operating performance that has badly trailed peers. The Company’s underperformance in this area has stood out for its unusually high operating expenses per barrel, a key industry metric that quantifies the efficiency of refining operations. Management should conduct a thorough review of the Company’s refining operations, with a view to greater cost discipline and higher profitability per barrel. Phillips 66 was once known as a top-tier operator with superb assets and a highly competitive position in the refining industry. Unfortunately, it has now lost this place of leadership in the market. Phillips 66 should commit to ambitious refining targets that reflect best-in-class performance and develop a credible path to achieving them.

- Enhanced oversight is also essential to a turnaround. After years of missed targets, management has lost the trust of Phillips 66’s investors, leading to the stock’s underperformance. For years, the Company has set operating and financial targets and then missed them, while claiming success. Investors no longer trust management and believe the Board has failed to hold management accountable for missed targets. The Company clearly needs stronger oversight to keep management on course. We believe that only by adding new independent directors can the Board deliver the accountability needed to oversee Phillips 66 management today and as the Company moves to execute on the first two steps of this plan.

At Phillips 66, Patience has been Punished

Eighteen months ago, we were willing to give the Company and its leaders a fair chance to restore Phillips 66 to best-in-class performance. We patiently supported them in their effort to do so. Unfortunately for investors, patience has been punished.

In the fall of 2023, we published a letter expressing our desire to work constructively with Phillips 66’s current management team, provided that it made significant progress toward the Company’s ambitious new targets. Our ask – a reasonable one – was that Phillips 66 add two new individuals with refining experience to its Board.

The rationale was that, after years of deteriorating execution, investors needed reassurance that there would be proper accountability and oversight of management – which, by its own admission, had taken its “eye off the ball” with respect to the Company’s core refining business.8 We also wrote that if Phillips 66 failed to show material progress to hit its targets, then we believed the Company should take an alternative path and embark on a transformation similar to the one undertaken by Marathon following our engagement there in 2019.

After initially agreeing to work with us to add two new directors to its Board, Phillips 66 reneged on that commitment. Instead, Phillips 66 added only one new director – Robert “Bob” Pease – after passing over a number of other highly qualified candidates whom we submitted for consideration.

We supported Mr. Pease’s appointment to the Board, in part because we were encouraged by his outlook on corporate governance. For example, during the interview process with us, Mr. Pease shared the very clear view that having a CEO also serve as Board Chair was detrimental to a company in need of change.

Yet, just one month after Mr. Pease joined the Board, he apparently voted to appoint CEO Mark Lashier to the position of Chairman as well – contrary to governance best practices and to the view he shared with us.

Allowing Mr. Lashier to consolidate control over the Company’s governance has hindered our ability to work constructively with Phillips 66 to improve the Company’s performance. Following Mr. Lashier’s appointment as Chairman, Phillips 66 failed to add a second director to its Board as promised – and not for a lack of effort on our part. Over the course of 2024, we provided management with the names of 10 strong independent candidates, including five former CEOs of prominent energy companies. Stubbornly, Phillips 66 refused to add any of these highly qualified individuals to the Company’s Board.

Nonetheless, we were patient – we gave management space as it tried to improve operations for more than a year. Finally, after a year of waiting and seeing no demonstrable progress, we concluded that Phillips 66 needed fundamental change – a significant Board refresh and a new plan to unlock the value trapped in the Company. We renewed our calls for change at Phillips 66 in February, while privately signaling to the Company our continued willingness to work constructively with the Board on the necessary changes.

In response, the Company stalled any in-person engagement with us for three weeks and refused to make any independent directors available for a meeting. Indeed, all of our attempts to engage with the Company’s independent directors – including direct outreach to Mr. Pease – have been turned away. Phillips 66 has insisted that we speak only with Mr. Lashier, his management team and his paid advisors, despite their unwillingness to consider meaningful change and their persistence in defending a status quo that is failing Phillips 66 shareholders. This sort of “engagement” is cosmetic, not substantive – and shareholders deserve the latter.

Most troubling of all, the Company’s leaders have claimed “success” on their turnaround efforts, despite falling woefully short of their stated goals. And to excuse the fact that this “success” has not been reflected in the Company’s languishing stock price, Mr. Lashier has reportedly been denigrating the value of Phillips 66’s enviable assets and competitive positioning – telling investors and analysts that their stock price is already “fairly valued” – a position that startled even seasoned industry analysts.9

At this point, it has become clear that sweeping changes are needed – changes to the Company’s structure, its operations and its Board.

While Phillips 66’s complacency has been frustrating to us and many other shareholders, the good news is that we all have a say in our Company’s future. The answer, we believe, is for the shareholders of Phillips 66 to make ourselves heard at the upcoming Annual Meeting by electing new members to the Board of Directors who are committed to productive change. We can send a message to Phillips 66 that we support bold actions to address our Company’s unrelenting underperformance. And we can endorse governance improvements to ensure that our Company’s leaders are accountable to shareholders in the future. As owners of Phillips 66, you should demand nothing less.

As Fellow Phillips 66 Shareholders, We Need Your Help

We’re not alone in our desire for bold change at Phillips 66: Since we first presented the “Streamline 66” plan on February 11, we have heard from many other experienced and sophisticated shareholders who share our frustrations and support the same path forward. Enacting this ambitious plan requires action from every shareholder ahead of the Company’s 2025 Annual Meeting in May. We strongly encourage you to vote on the Gold Card for Elliott’s outstanding slate of director nominees and for the governance enhancements we have proposed.

Phillips 66’s response to our case for change – alternately misrepresenting our critiques and overstating its own performance – has only added to the impression that a fresh lineup on the Board is in order. For starters, the Board of the third-largest independent refiner in the U.S., with significant midstream assets, should have a wealth of refining and midstream experience. Instead, the current Board is made up of individuals with backgrounds in aerospace, airlines, food and beverage companies, commercial retail, and investment research.

By contrast, the director candidates we support would add urgently needed experience and valuable new perspectives:

- Sigmund Cornelius served as CFO at the predecessor company of Phillips 66, ConocoPhillips, where he oversaw a substantial divestiture and simplification program that led to a material increase in shareholder value. He later served as president of Freeport LNG Development, as well as a director at Andeavor and Western Refining.

- Michael Heim has a long record of leadership in the industry as a founder of Targa Resources, one of the most successful Permian-focused midstream operators, and as a member of multiple boards and a respected consultant.

- Brian Coffman is a seasoned operator who spent much of his career running Phillips 66’s current refining assets while they were part of ConocoPhillips. After three decades at ConocoPhillips, he became the executive in charge of refining for Andeavor, leading the operations of ten refineries throughout the United States, as well as the President and CEO of Motiva, one of North America’s largest refiners.

- Stacy Nieuwoudt would bring an investor’s eye to Phillips 66’s challenges, having spent her career as a senior energy and industrials analyst at Citadel. She has also served on the boards of multiple publicly traded energy companies.

As directors, these nominees will bring experience, independence, relevant insight, judgment and objectivity to a boardroom that has clearly been lacking these strengths. Shareholders will know that the Board of Phillips 66 is fully equipped to keep management on mission and to hold that team accountable for results.

Just as important, a board that upholds accountability should itself be accountable. Elliott is proposing a key improvement to Phillips 66’s corporate governance: annual elections for all Board seats, rather than the current arrangement of a staggered Board with only a portion of seats up for election each year.

Staggered boards are not in the interest of shareholders, because they limit accountability and can enable entrenchment. Proposals to address this defect have been presented at past Phillips 66 Annual Meetings and have consistently received near-unanimous support among those shareholders who have voted. However, these measures have never passed, because amendments to the Company’s charter must be supported by 80% of all outstanding shares – not just voted shares – and this threshold is all but impossible to meet.

To overcome this obstacle, we have proposed a straightforward way for the Board to promote the annual election of all directors: a non-binding proposal calling for each director to commit to a one-year term and stand for election at each Annual Meeting. This policy reflects standard best practice in corporate governance, and it is what the vast majority of Phillips 66 shareholders want – as evidenced by the 99% of voting shareholders who supported de-staggering the last time it was proposed. The policy would make all directors accountable to shareholders, each year.

Incredibly, Phillips 66’s leaders have come out against this proposal, arguing that this measure could potentially conflict with the Company’s governing documents. This argument is entirely unconvincing, however, because the proposal is non-binding, and compliance with it would be voluntary – requiring only that all Phillips 66 directors have the courage to be accountable to shareholders on an annual basis, as is the case at nearly 90% of the companies in the S&P 500.10

Instead, the Company is asking shareholders to try the same approach to de-staggering that has repeatedly failed before – fully aware that its supermajority voting requirement makes failing again a near certainty. Shareholders should be asking whether a Board truly interested in good governance would be satisfied with this status quo, allowing an archaic governance regime to constrain shareholder choice and shield a majority of its directors, who have presided over years of underperformance, from an annual shareholder vote.

By contrast, all of the nominees on the Gold Card have committed to abide by this important and shareholder-friendly reform. As directors, they would gladly and confidently answer to shareholders every year.

Vote Your Shares on the Gold Card to Put a Phillips 66 Turnaround into Action

More information about each of our candidates is included with this letter, along with further details on our “Streamline 66” plan (also available at Streamline66.com). If you have questions, please contact us at [email protected] or at (877) 629-6357. We hope you’ll stay engaged as this crucial vote draws near – a lot rides on the outcome, and every vote matters.

We are all investors in a once-respected company that could and should be doing far better and earning far more than its current leadership would have you believe possible. In this election, shareholders have a clear choice: On the one hand, there is the vision of Mr. Lashier, according to which Phillips 66 is already doing as well as possible and is fully valued now, even as it delivers worst-in-class returns, year after year.

Or there is the vision outlined in this letter and represented by the Gold Card – a path to a dramatically higher stock price and a Board capable of ensuring that these higher returns are sustained for the long term.

We at Elliott have studied the unmet potential and immense opportunities at Phillips 66. Making this company the best it can be – with a focus on core strengths and operational discipline, overseen by an adept and energetic Board – offers the possibility of a stronger, more valuable Phillips 66 for all of its investors.

We’re eager to get moving on this decisive turnaround, and we ask for your support on the enclosed Gold Card.

Respectfully,

Elliott Investment Management

1 Total Shareholder Return per Bloomberg, ending on 2/7/25.

2Total Shareholder Return relative to the average of Valero and Marathon, per Bloomberg, ending on 2/7/25.

3Per Bloomberg as of 2/7/25.

4Total Shareholder Return relative to the average of Valero and Phillips 66, per Bloomberg, ending on 2/7/25.

5Price target is based on Elliott’s internal calculations.

6Price target is based on Elliott’s internal calculations.

7Midstream valuation based on Elliott’s internal calculations.

8Mark Lashier (CEO), January 2023, GS Energy Conference.

9“In a somewhat surprising tactic, PSX management talked down the potential [sum-of-the-parts] upside (i.e., [stating that the Company is] fairly valued)….” – Piper Sandler, March 2025.

10Source: FactSet as of 4/3/2025.

(a)Unaffected stock price per Bloomberg as of 2/7/25, just prior to the publication of Elliott’s ”Streamline 66” plan.

(b)Price target is based on Elliott’s internal calculations.

ADDITIONAL INFORMATION

Elliott Investment Management L.P., together with the other participants in Elliott’s proxy solicitation (collectively, “Elliott”), has filed a definitive proxy statement and accompanying GOLD universal proxy card with the Securities and Exchange Commission (“SEC”) to be used to solicit proxies with respect to the election of Elliott’s slate of highly qualified director candidates and the other proposals to be presented at the 2025 annual meeting of stockholders (the “Annual Meeting”) of Phillips 66, a Delaware corporation (“Phillips” or the “Company”). Stockholders are advised to read the proxy statement and any other documents related to the solicitation of stockholders of the Company in connection with the Annual Meeting because they contain important information, including information relating to the participants in Elliott’s proxy solicitation. These materials and other materials filed by Elliott with the SEC in connection with the solicitation of proxies are available at no charge on the SEC’s website at http://www.sec.gov. The definitive proxy statement and other relevant documents filed by Elliott with the SEC are also available, without charge, by directing a request to Elliott’s proxy solicitor, Okapi Partners LLC, at its toll-free number (877) 629-6357 or via email at [email protected].

About Elliott

Elliott Investment Management L.P. (together with its affiliates, “Elliott”) manages approximately $72.7 billion of assets as of December 31, 2024. Founded in 1977, it is one of the oldest funds under continuous management. The Elliott funds’ investors include pension plans, sovereign wealth funds, endowments, foundations, funds-of-funds, high net worth individuals and families, and employees of the firm.